Trading in single-name credit default swaps is booming this year as higher interest rates and market turmoil have triggered a surge in demand for the controversial derivatives contracts.

Single-name CDS volumes are up 30% so far this year, according to post-trade firm OSTTRA, with activity linked to global systematically important banks rocketing 125% following the collapse of Silicon Valley Bank and UBS's emergency rescue of Credit Suisse in March. That rebound has also put these derivatives back on regulators' radar after European policymakers blamed the instruments for exacerbating turmoil in the banking sector.

Such warnings have done little to dent the appeal of the instruments among many traders and investors. Higher interest rates have attracted more money into fixed-income investments more broadly, while also stoking demand to hedge against debt defaults and prompting hedge funds to ramp up bets against struggling companies.

"When the market is stressed and volatile, then there's a lot more demand for [CDS] protection," said Laurent Samama, head of flow credit trading for Europe at BNP Paribas. "There's been plenty of volatility in the market this year to necessitate single-name CDS trading, especially around financials."

Trading in derivatives insuring against individual companies defaulting on their debts has declined sharply since the market's heyday in 2007. Back then, banks cramming single-name CDS into complex financial products such as synthetic collateralised debt obligations caused the overall amount of CDS outstanding to swell to US$61trn.

The complexion of the market has changed dramatically over the last 15 years as demand for synthetic CDOs has waned and CDS has become better regulated. Single-name CDS accounted for just over 40% of the US$9.8trn of total CDS outstanding at the end of last year, according to the Bank for International Settlements – with broad-based indices proving a more popular instrument among investors hedging macro risks.

The single-name market has also become far more concentrated. Just 30 names are responsible for a third or more of CDS volumes each month, according to trade body ISDA. Sovereign CDS are usually the most-traded contracts, remaining a staple with investors hedging events such as the US debt ceiling drama or Russia's debt default last year. This year, though, activity has broadened to other credits as central banks' aggressive interest rate hikes have rocked bond markets.

Rising rates mean "bonds become more attractive for investors, which may increase demand for hedging", said Jonathan Martin, head of derivatives products management at ISDA. There's also more risk that companies could go bankrupt, "which makes single-name CDS more relevant" as a hedging tool, Martin said.

Hitting a peak

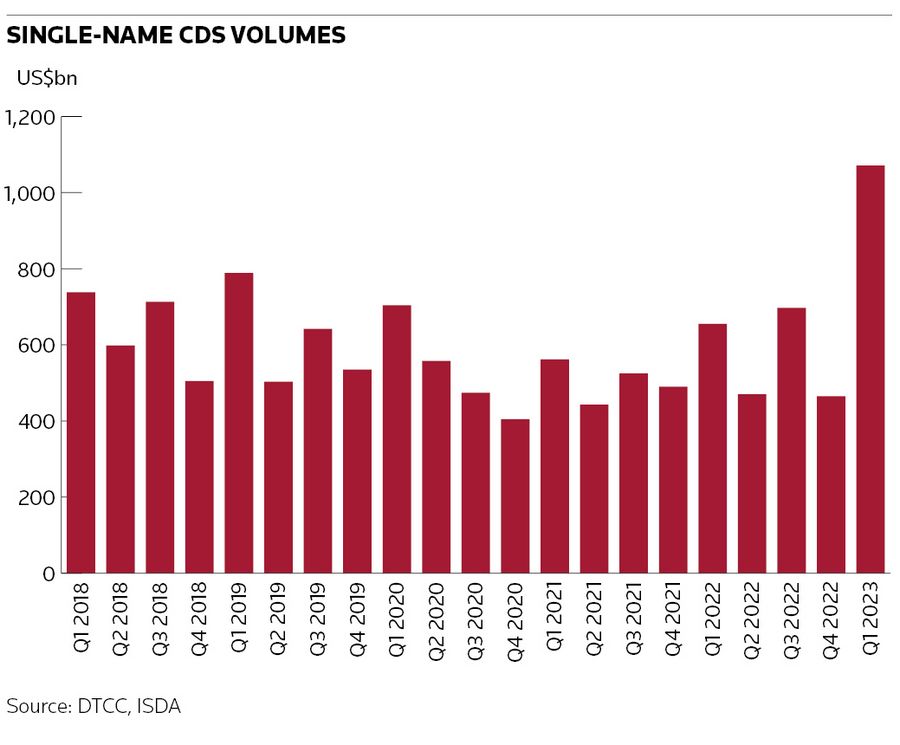

Single-name volumes peaked at a five-year high of US$1.1trn in the first quarter, a period when European users also had to navigate significant upheaval in the financial plumbing underpinning these markets. ICE Clear Europe began shuttering its CDS central clearinghouse around that time, forcing a mass migration of positions to ICE's US clearing unit as well as to LCH's European clearinghouse, CDSClear.

CDSClear has seen a 115% increase in cleared notional for European single-names, while cleared notional for US names has grown 16 times in 2023. But executives say that's not all down to the clearinghouse transition. For example, record numbers of people rolled their positions into the newest CDS contracts when they were launched in September, said Adam Johnson, head of product development at CDSClear.

"Even if we put [the clearinghouse migration] aside, we've been seeing big volumes in single-names this year due to the macroeconomic environment," said Johnson. LCH is part of LSEG, which also owns IFR.

Banks remain the most active user of single-name CDS as they hedge exposure stemming from their derivatives and loan portfolios. But traders say hedge funds and asset managers have also been heavily involved this year, either by hedging or betting against troubled companies. The banking crisis in March triggered a flurry of hedging activity, while hedge funds have also zeroed in on companies that tend to suffer when economies slow – such as those in the chemicals, and paper and packaging sectors.

"The last time we saw similar levels of activity was 2020 when Covid hit and a lot of investors, banks and hedge funds had a real need for this product to hedge the stress they were facing in the market," said Davy Kim, North America head of credit macro trading at Citigroup. "A similar story is happening this year, which is why volumes have picked up."

Some of that activity has caught the attention of European policymakers, who have long taken a dim view of the credit derivatives market. The near collapse of Credit Suisse in March led to a sharp increase in the cost of default insurance on other European lenders, with CDS on Deutsche Bank briefly spiralling higher.

Unfairly scapegoated?

Regulators raised concerns that CDS moves could have fuelled a sharp sell-off in Deutsche's share price and called for further reforms of the market. Many credit traders are dismissive of such theories, instead suggesting that the CDS market has been unfairly maligned for jitters in the wider financial system.

"Throughout the volatile events of the last few years, the CDS market was functioning, resilient, and proved – again – that there was liquidity and volume," said BNPP's Samama, without directly commenting on the Credit Suisse and Deutsche events. "We have generally observed a rational repricing of spreads, and the CDS market was not sending a very different signal than the one coming from the bond market during these times."

Despite the broader trading increase, there's no doubt that the noise surrounding the CDS market remains off-putting for some investors. "Not everyone wants to use CDS or likes to use CDS," said Nachu Chockalingam, a senior portfolio manager at Federated Hermes, who said many fund managers simply won't touch the instruments.

For her, the market still offers interesting opportunities, such as discrepancies that have emerged between single-name contracts and broader CDS indices. "Single-name CDS has become quite an important investment tool for us this year," Chockalingam said.