The increasing dominance of renminbi-denominated funds in China’s private equity market is expected to lead to more Chinese companies listing domestically instead of overseas, adding more challenges to the Hong Kong IPO market.

China’s PE market has traditionally been led by renminbi funds but their share has significantly increased versus US dollar funds since 2021 as a regulatory clampdown on the technology sector and escalating tensions with the US have discouraged US investors from deploying capital in the country.

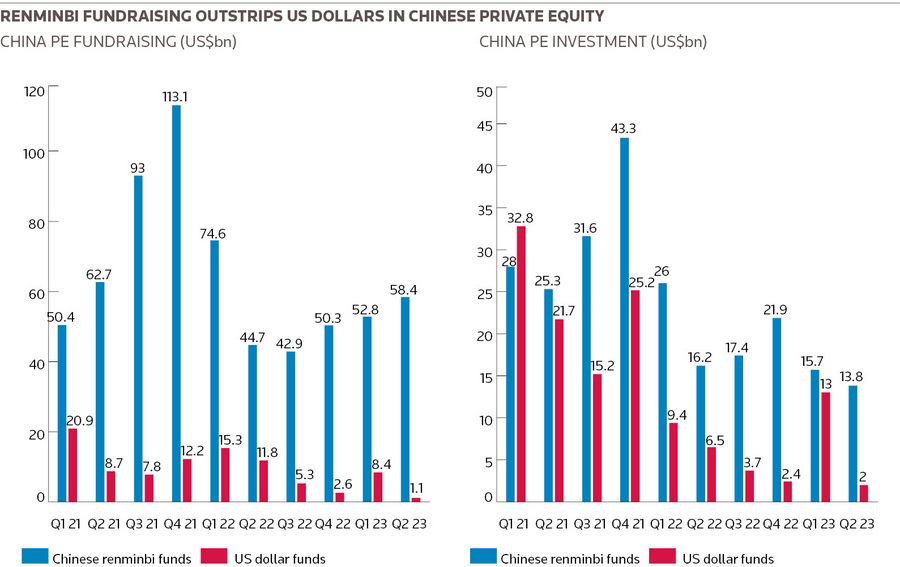

The imbalance became even more obvious in the second quarter of this year. According to a report by investment bank China Renaissance, renminbi-denominated funds raised US$58.4bn in the three months to June 30, which accounted for 98% of China’s private equity fundraising market, the highest proportion in five years. US dollar funds raised just US$1.1bn.

Renminbi funds invested US$13.8bn in the quarter, while US dollar funds deployed US$2bn.

“The trend is worrying,” said a Hong Kong-based banker. “Almost all the private equity investments now are in renminbi, which means Chinese companies don’t really have a reason to list overseas in Hong Kong or the US.”

Allowing foreign investors to exit has been one of the key reasons for Chinese companies to list offshore.

The trend is likely to continue after US president Joe Biden on Wednesday signed an executive order that will prohibit US private equity and venture capital firms from investing in China in sensitive technologies such as semiconductors and microelectronics, quantum information technologies and certain artificial intelligence systems.

The US said the order is aimed at protecting national security and preventing US capital from helping China develop cutting-edge technologies that could improve its military capabilities.

Mixed factors

A range of factors has driven the rise of renminbi investments and the fall of US dollar investments, according to private equity investors and bankers. They all agree, however, that Sino-US tensions are the main reason.

Startups in the technology, media, and telecoms space, which were once the most sought-after targets by PE or venture capital firms, are no longer favoured.

Instead, so-called hard-and-core technology companies such as semiconductor makers have drawn strong investments from local money as Beijing is encouraging the development of homegrown technology – driven partly by a US ban on exports of certain high-tech materials to Chinese chipmakers.

“Due to the sensitivity of their business, those hard-and-core companies are definitely not going to list in the US. From day one, they only accept renminbi investments,” said a Shanghai-based PE investor.

“If they accept US dollar investments, it will be disadvantageous for them to continue doing business with government entities such as military and state-owned enterprises.”

According to another Hong Kong-based banker, some Chinese companies prefer renminbi investments even though they can also accept US dollars. “We tried to line up a US dollar PE investment for a Sino-foreign joint venture but the management told us they prefer to take renminbi as it’s seen as more politically correct,” said the banker.

Against this backdrop, state-owned investment firms have unsurprisingly become the main investors in the PE market. In the second quarter, 75% of the renminbi funds that raised more than Rmb1bn (US$139m) each were backed by state-owned players, according to the China Renaissance report.

In the first half of this year, the most active investor by number of deals was Addor Capital, followed by Shenzhen Venture Capital, Shenzhen HTI Group, Sequoia Capital and State Power Investment Corp. Apart from Sequoia, the rest are all backed by local governments.

IPO exit

The fact that US IPOs are no longer the exit of choice for private equity firms also makes investors less eager to invest US dollars in Chinese companies.

Chinese regulators have tightened scrutiny on overseas listings since ride-hailing provider Didi Global upset them with its US$4.4bn US IPO in June 2021. Even though regulators said they would allow companies with variable interest entity structures to list overseas, approvals for such companies have been slow in coming.

An investor relations official at a China-focused PE firm that used to raise only US dollars said it has been raising less in the currency in recent years.

“Our GPs [general partners] are mostly overseas high-net-worth individuals. Last year, we didn’t raise any US dollars at all and only raised some renminbi. I think the main reason is the GPs are not satisfied with our exit performance as the channel to list in the US is not very smooth,” said the official.

Hong Kong's IPO market is also suffering. The city, which used to be one of the world’s top three listing venues, has slid to ninth after fundraising fell to a 20-year low in the first half.

In contrast, the pace of A-share IPOs has accelerated since China rolled out a registration-based system in February to all its stock markets. IPOs on the Shanghai and Shenzhen exchanges raised a combined US$32bn in the first half, making China the world’s top IPO market.

“Chinese companies are the main source of supply for the Hong Kong IPO market. If more and more Chinese companies receive renminbi PE investments and opt for domestic listings, Hong Kong will further lose its charm as an international fundraising centre,” said a third Hong Kong-based banker.