A jump in demand for interest rate hedges has bolstered volumes this year of a risky type of derivative designed to shield companies against adverse market moves around the time of acquisitions and other corporate deals.

Client demand for deal contingent interest rate hedges has almost tripled since 2022, according to hedging advisory firm Chatham Financial, despite a severe slump in global M&A deals that many thought would dampen interest in these complex derivatives.

The uptick in activity is the latest sign of how companies and investors are looking to lock in their future borrowing costs as central banks raise interest rates at the fastest pace in years.

"Given such heightened market volatility, we are seeing increased demand for deal contingent hedging solutions from our clients in almost every region," said Christian Banna, head of Santander's UK risk solutions group.

Walk away

Deal contingents are a type of derivative that companies and investors use to hedge against moves in currencies or interest rates between announcing a deal and when it closes. The best part for the client is that they can walk away without paying for the hedge if the deal falls through, whether that's a botched cross-border acquisition, a debt raise or an abortive company delisting – to take just three examples.

That flexibility makes these trades fraught with risks for the banks that provide them. If the deal fails and the market moves against the bank, it can find itself on the hook for sizeable losses. That happened last year when Barclays took a US$125m hit on a deal contingent trade.

To account for these risks, banks charge clients a premium that is calculated using the cost of the relevant FX or interest rate option. Riskier deals with a higher chance of failing typically carry a heftier price tag.

Deal contingents have long been popular with cost-conscious private equity investors mindful of currency swings squeezing their returns on cross-border deals. But interest rate deal contingents have become increasingly commonplace in recent years as more companies look to fix borrowing costs on takeovers and financings.

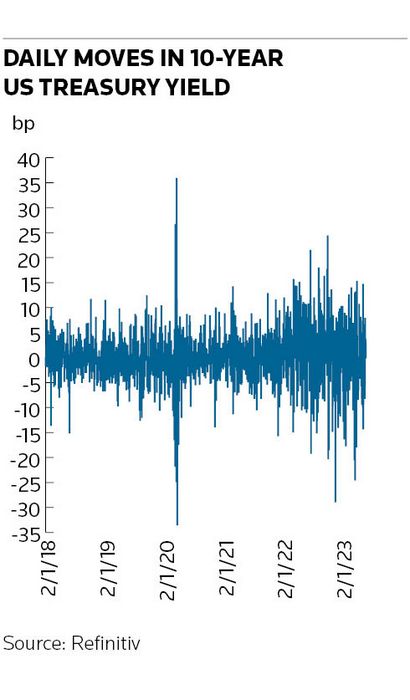

That trend has accelerated as bond market volatility has rocketed in response to central banks raising interest rates. Banna noted that the 10-year Treasury yield moved more than 10bp in a day on only 28 occasions between 2013 and 2021. That increased to 153 times last year and has already happened 136 times in 2023.

"The current interest rate environment has been a complete game-changer for pre-hedging solutions such as deal contingents," said another senior European banker.

Jackie Bowie, Chatham Financial's head of EMEA, said she used to see around one interest rate deal contingent hedge for every 10 FX deal contingent hedges when rates were near zero. Today, that ratio has flipped, she said.

M&A slump

The rise in demand has come despite a slump in M&A volume – the deals that usually underpin the need for deal contingent hedges. Global announced M&A deal volume fell 42% to US$597bn in the first quarter from a year earlier, according to Refinitiv data, marking the worst start to a year since 2013. Despite that slowdown, bankers say a larger share of those involved in M&A deals are looking to pre-hedge their debt financing costs with contingent derivatives.

"One effect is essentially balancing out the other," said the senior European banker, who added that the proportion of M&A situations in which a deal contingent trade is attached is greater than before.

Interest rates are "now the main risk keeping you up at night, which wasn't the case just a few months ago", the banker added.

The rise in interest rate deal contingents has also come despite the increased cost of doing these hedges, said Benoit Duhil de Benaze, managing director of the European private equity team at Chatham Financial. He said the higher costs are due to a decline in the number of banks involved in the underlying transactions – whether as advisers or debt underwriters – shrinking the pool of "natural counterparties" to provide the hedge.

Double dealing

Banks active in underwriting deal contingent transactions are also taking advantage of growing demand to upsell clients with a combined FX and rates hedge – a so-called double-deal contingent trade. Such deals would be attractive for, say, a US-based client acquiring a European company that needs to hedge its FX risk (switching from US dollars to euros to buy the asset) and its rates risk (related to borrowing in euros) to finance part of the purchase.

According to Banna, these double-deal contingents should allow banks to offer clients lower hedging prices than would otherwise be achieved – in part, because of the potential netting efficiencies between FX and interest rate markets.

However, Duhil de Benaze at Chatham – which runs competitive bids between banks on deal contingent trades for clients – said separating the interest rate and FX hedges is typically the cheapest option for clients.

"When we create competitive tension between banks, the ultimate allocation of the trade might be to give the FX deal contingent hedge to one bank and the rates hedge to another as that's usually the way to achieve the best pricing for the client," he said.