Banco de Sabadell and NN Bank attacked the short end with covered bonds on Tuesday, as active issuers enjoy the fruits of substantial demand and pricing leverage.

"The market is there, it’s strong, secondary spreads are tightening," said a banker.

"I’m surprised to not have seen more supply in the last couple of days. Maybe today’s outcomes will now be a wake-up call for other issuers. Whoever is considering it should just come to the market. I would even go further and say it’s not only the front end – where investors are – which is working, picking a longer tenor would also work."

Sabadell paid no new issue premium for a €1bn August 2026 soft-bullet cedulas hipotecarias which was met with over €4.25bn of demand. Banco Sabadell, Barclays, Commerzbank, JP Morgan, Natixis and UniCredit opened books at mid-swaps plus 32bp area and set the final spread at 25bp.

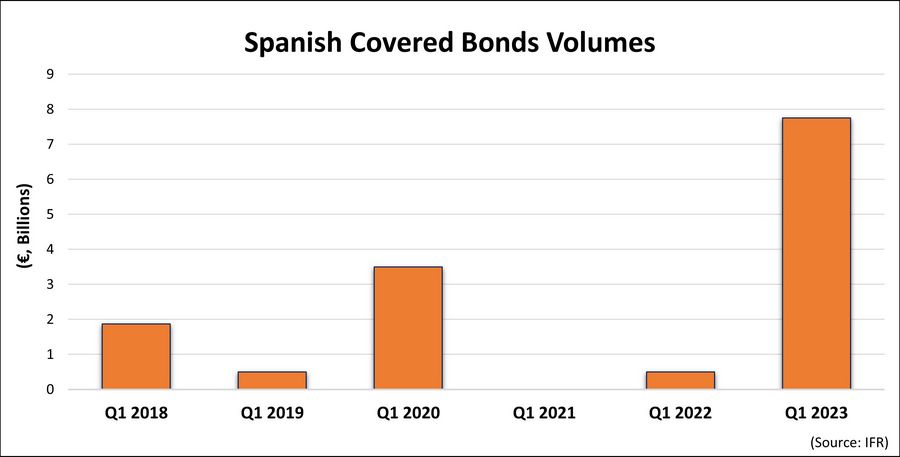

“The tenor was really fitting for investors – we were able to move 7bp, which not many of us had thought of this morning," the banker said. "We have a very small gap to national champions BBVA and Santander, which shows the quality of the name, the appreciation of the tenor, plus the rarity of Spanish cedulas, which haven’t been issued so much in the last couple of years.”

A second banker said the success of the trade was a reflection not only of the high quality of the issuer's name but of the decent spread on offer in a context where investors are expecting a tightening in spreads.

"Maybe it will be short-lived but we definitely see the market is in a repricing mood now, so primaries are repricing secondaries to the tighter end," said the second banker.

"Liquidity is still out there and covereds are still sought-after compared to SSAs and even credit and financials as well. They seem to be very cheap at the moment, if you have senior preferreds of BHH et cetera or even non-preferreds trading in single-digit territory and sometimes negative territory versus mid-swaps, when covered bonds are coming in positive double-digit territory like today."

NN Bank’s €750m May 2027 mortgage-backed green bond was more than twice subscribed. It was the second green covered issue by the Dutch Bank, which to date is the only issuer to have printed ESG-labelled covered debt out of the Netherlands.

“We knew it would go well but a €2bn book is not the base case expectation in terms of demand,” the second banker said. “The greenium always helps if you look at accounts which are playing. It was a decisive aspect for this transaction.”

ABN AMRO, Deutsche Bank, HSBC, LBBW, Rabobank and Societe Generale began marketing the soft-bullet notes at mid-swaps plus 14bp area.

The leads landed the trade at 10bp, conceding 1bp of new issue premium.

“A 9bp landing would have also been possible but the final pricing was fair," the second banker said. "The issuer is not overstretching because they know how difficult markets were in 2022."

With the public pipeline looking thin, Tuesday's covered bonds were among the last to be eligible for ECB primary purchases, though market participants pointed out that the ECB bid has had minimal impact on trades of this size and with such levels of demand.

“It’s still buying with 10% but it doesn’t count for much," said the second banker. "It wouldn’t change the pricing at all. From this week onwards, they would be dropping to zero for deals with settlements going into March.”