The International Swaps and Derivatives Association is lobbying for a lower risk weighting for carbon credits to encourage more banks to participate in carbon trading and free up financing for the energy transition.

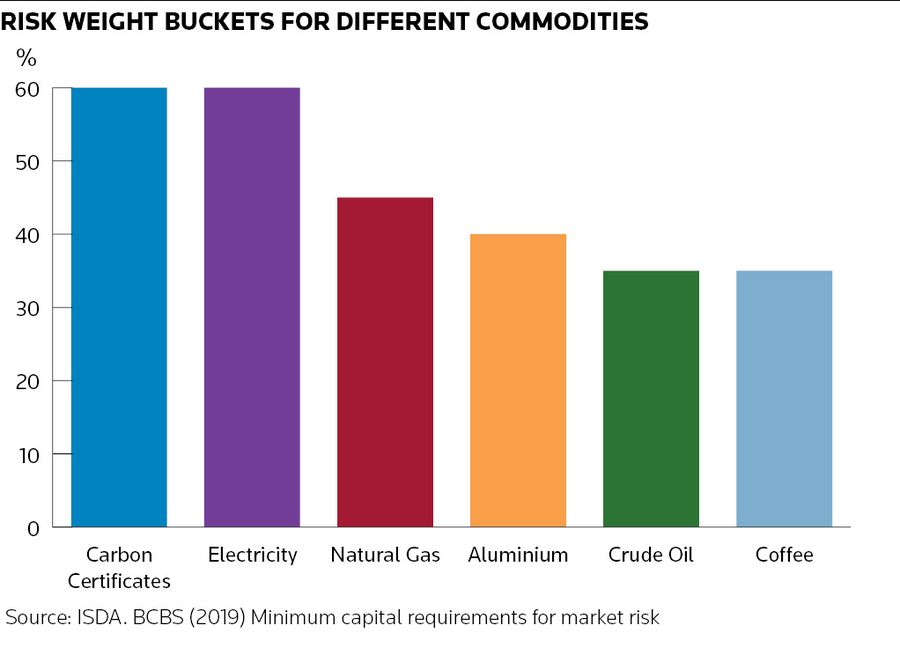

Carbon credits attract a 60% risk weighting under the Fundamental Review of the Trading Book rules being introduced under the Basel III framework – one of the highest ratios for any commodity.

That will tie up substantial amounts of banks' capital and deter them from trading carbon credits, reducing funding for the energy transition and slowing the development of carbon markets.

“The conservatism of Basel III capital requirements for carbon credits could impair the ability of banks to support the transition to a sustainable economy,” said Scott O’Malia, ISDA’s chief executive officer.

The ongoing transition to the FRTB standard is already creating issues. Many banks are currently using internal models to price carbon and are facing a steep rise in capital allocation as they move to calculate and produce the FRTB’s standardised approach as part of their disclosure requirements.

The move to the FRTB rules comes just as banks are starting to build carbon-trading businesses. In February, BNP Paribas, UBS and Standard Chartered joined Carbonplace, a settlement platform for carbon credit trading which was set up by CIBC, Itau Unibanco, National Australia Bank and NatWest in July 2021.

And the new rules put such participation in jeopardy. "A risk-appropriate and risk-sensitive framework is critical for banks to continue participating in this market," said Gregg Jones, risk and capital director at ISDA.

Lower weighting

ISDA argues that an analysis of historical data in the mandatory carbon markets suggests the risk weighting for carbon credits should be 37%.

That analysis is based on the European Union Emissions Trading System, which makes up 80% of all carbon trading, plus the two North American markets (the Western Climate Initiative and the Regional Greenhouse Gas Initiative) and the UK's Emissions Trading Scheme.

ISDA’s lower risk-weighting figure is supported by the EU’s legislative proposal for the third Capital Requirements Regulation, which was published in October 2021 and recommended that the risk weighting for carbon should be reduced to 40%.

The FRTB’s 60% risk weighting currently also applies to the voluntary carbon market, which is at an earlier stage of development than the more established mandatory markets and has very different characteristics.

The voluntary market helps companies and organisations to meet net-zero targets by offsetting emissions that may be difficult or impossible to eliminate from their supply chains. Companies typically buy voluntary carbon credits to retire an equivalent amount of CO2 emissions.

"When we look at the revised market-risk framework, there is currently a single bucket prescribed for carbon credits," said Panayiotis Dionysopoulos, head of capital at ISDA. "The question is, what would the appropriate parameters be if there are differences between the compliance market and the voluntary carbon credit market? We don't have enough data to perform similar analysis for the voluntary carbon credit market. More research will be needed."

Effective intervention?

Key jurisdictions are developing legislation that will transpose Basel III into law and ISDA is hoping for some additional changes before the FRTB rules are finally implemented.

The FRTB rules also impose a carbon capital charge for buying spot and selling forward by applying a correlation that includes the fluctuating costs of storing commodities, despite the fact that there are no physical storage costs for carbon credits.

ISDA is therefore arguing for a different correlation structure between tenors, which is essentially the carry position where banks buy short and sell long, to better reflect the specifics of carbon credits.

"If you have a hedged position, you're running low risk and should have the appropriate capital attached to that," Dionysopoulos said.

The trade body is hoping that its call for lower risk weighting, a tenor-based correlation structure and greater international consistency of implementation will be heeded to free up more capital to fund the energy transition.

“We urge EU officials and politicians to support this proposal, and we believe it should be replicated in other jurisdictions to ensure an appropriate and consistent approach to this market,” O’Malia said.