![]()

![]()

![]()

![]()

In the autumn of 1962, English banker George Bolton went on a business trip to New York. As chairman of a European bank – in his case the Bank of London and South America – regular trips to the US were an essential part of the job. Since the World War II, the country had become the place for European governments and companies to raise the funds they needed. In the years since the end of the conflict, they had raised billions of dollars by selling bonds to US investors.

But during his business trip, Bolton made a startling discovery. He learned that plans were afoot to cut off the Europeans from this vital supply of dollars. Washington had quietly requested that the big US banks stop lending to European borrowers in a bid to stem the huge outflows of currency from the country that were threatening the stability of the US dollar. “If methods of persuasion fail, I would not exclude legislation,” Bolton wrote despondently on his return to London.

The discovery created an urgency to bypass New York and find an alternative way for European borrowers to access the dollars they vitally needed. It kick-started a race, led by a group of Jewish emigres who had fled the Nazis and re-established themselves in London, but who were finding it difficult to break into the City's clubby networks. Spotting an opportunity to carve out their own niche, they hit on the idea of tapping the growing piles of stateless dollars being built outside the US.

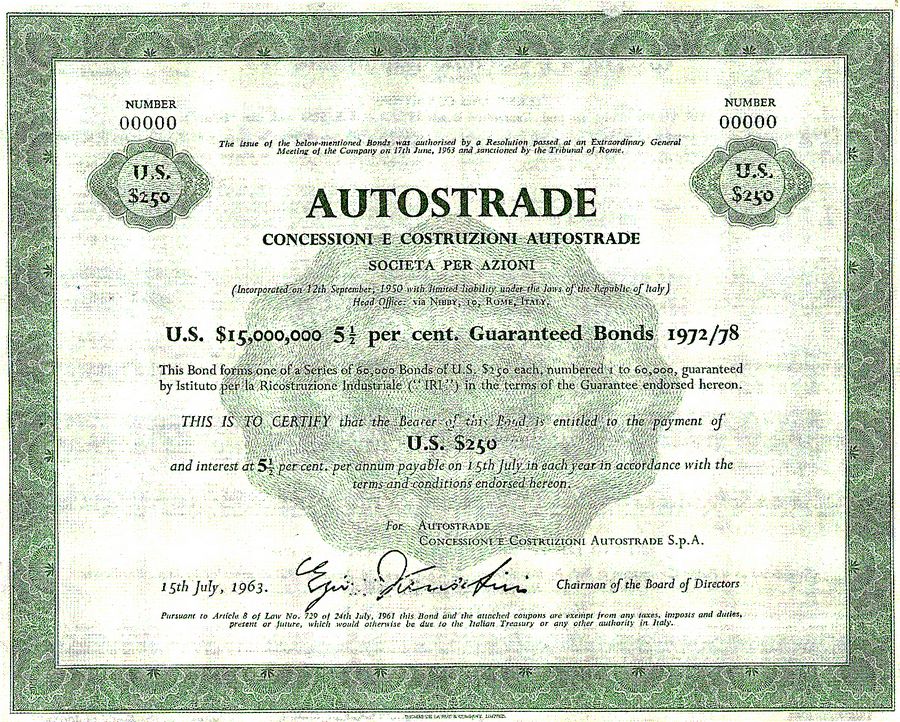

This is the story of how a small group of visionaries would transform global financial markets forever. In the process these foreign outsiders would help London to regain its crown as the world’s financial capital. It’s the story of how they convinced the relatively unknown Italian motorway operator Autostrade to take a gamble on their new idea, the Eurobond, and in the process helped create a market that today is worth around US$30trn.

But to get there they had to overcome a host of problems. First, there were UK laws that prohibited residents from lending their money to foreigners, which would massively restrict business in Eurobonds. There were rules against buying bearer securities, the format of the deal. There was also the problem of a listing – most banks couldn’t underwrite bonds unless they were listed on a major exchange. But the creativity of the Eurobond pioneers overcame these hurdles to make the deal a huge success.

And yet none of the pioneers were prepared for what would come next. Within two weeks of the deal being done, the Kennedy administration announced new bond market rules that were far stricter than anyone had imagined. The announcement dropped a bombshell on the Yankee market. With that one measure, the Kennedy administration effectively killed the New York foreign bond market and pushed issuance to the new Eurobond market in London.

As the news came through, the chairman of Morgan Guaranty in New York, Henry Alexander, shared his concern with colleagues. “This is a day that you will remember forever,” he said. “It will change the face of American banking and force all the business off to London. It will take years to get rid of this legislation.” He was right. The cost of the Vietnam War would mean that restrictions on foreign borrowers would remain until 1974. By then, London was years ahead.

To hear this episode – and more like it – for free and in full, click one of the links below or search your podcast provider of choice for "IFR the Syndicate".

![]()

![]()

![]()

![]()