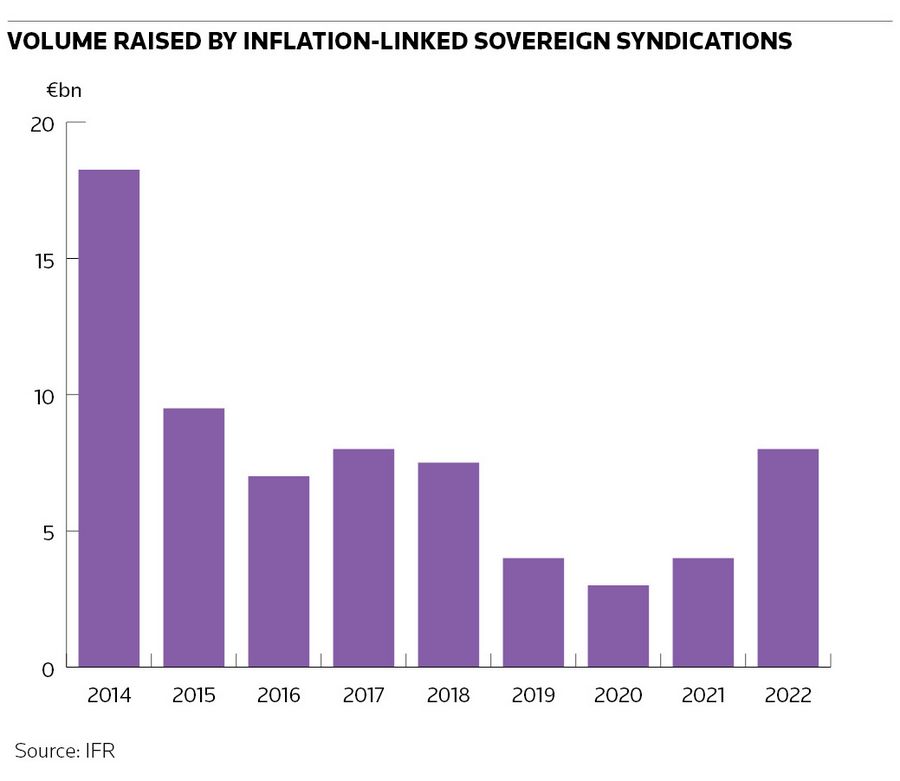

Italy sold the biggest syndicated inflation-linked bond in the euro market in nearly five years last week as sovereigns react to soaring prices, encouraged by growing demand for the product.

Italy's €5bn 10-year bond on Wednesday was the second such deal by a sovereign in quick succession, after France began its issuance for 2022 with a €3bn 30-year linker on January 25. The total amount raised by the two deals is already greater than linker issuance volumes in the euro market in each of the last three years. And with inflationary pressures heightening, more supply is expected over the coming months. France is considering a green linker, while Spain and Germany are also expected to sell linkers either via syndication or auction.

“The market has definitely changed. It is no longer the market of 2018 or 2019. The investment community that is interested in these type of products is very keen on getting protection from inflation and looks to deals like these because of their liquidity," said Michele Cortese, head of Italian DCM at Societe Generale, a lead bank on both the France and Italy transactions.

With the latest consumer price inflation data in the eurozone revealing an annualised rise of 5.1% in January, well above the consensus forecast of 4.4%, demand for linkers is only likely to become greater.

"Demand for inflation strategies has always been cyclical. As peak inflation continues to be revised higher and pushed further into the future, the market should remain fairly hot," said Jonathan Baltora, head of sovereign, inflation and FX, at AXA Investment Managers.

Italy capitalised on the hot market by launching the deal just days after Sergio Mattarella's reelection as president ended several weeks of political uncertainty. Mattarella's second term, which was confirmed on January 30, left Mario Draghi as prime minister, a move welcomed by investors.

Italy (Baa3/BBB/BBB/BBB high; Moody's, S&P, Fitch, DBRS) opened books on the May 2033 BTPei at 36bp over the 0.4% May 2030 BTPei before pricing the deal at plus 34bp. That meant a 1bp concession as orders reached over €18.75bn (including €1.45bn of leads' interest). It was the biggest linker in the euro market since Spain sold a €5bn deal in April 2017 through a November 2027 note.

“The size was on the upper end for linker transactions," said Davide Iacovoni, general manager of public debt at the treasury department of Italy's Ministry of Economy and Finance.

"There were a lot of very good quality long-term investors in the book. Some of these guys were probably jumping back into the market for linkers because of this new inflation environment. We also saw a lot of new demand, especially from the world of insurance and pension funds."

Showing the way

France (Aa2/AA/AA/AA high) had already shown the depth and breadth of demand for linkers after books for its July 2053 OAT€i had closed in excess of €23.5bn (including €2.95bn of leads' interest). “When we looked at the investor base for this deal it had clearly expanded, likely due to inflation being such a key narrative right now," said Cyril Rousseau, chief executive of Agence France Tresor. "We usually have a little over 100 investors for linker syndications but we were close to 200 for this syndication."

While many investors are buying linkers as a hedge against rising inflation, that's not the only strategy. The development of asset-swap transactions, where investors buy an inflation-linked bond and sell the inflation component in order to obtain a fixed-rate outcome, has also contributed to the rise in demand, according to Baltora, who noted market talk of large asset-swap demand for the French 30-year OAT€i.

"The positive of such transactions for issuers is that investors that do not particularly need to hedge inflation are often taking part. Asset-swap transactions have become mainstream and the 'asset swap metric' has become a key relative value indicator just like the inflation breakeven. A wide asset swap metric would suggest that inflation-hedged OAT€is, for instance, are cheap to nominals," Baltora said.

Sweet spot

What's making the opportunity for linkers especially attractive at the moment is a set of market conditions that suits both issuers and investors. However, if inflation continues to spike up then issuers will have little incentive to continue issuance as the cost of debt service payments will increase substantially.

“For sovereigns it is a perfect opportunity to test the temporary inflation narrative," said Asif Sherani, head of DCM syndicate for EMEA at HSBC. "If they believe, like many economists and central bankers, that inflation around these levels will be short-lived, issuing in a market where prints are high but will eventually fall back down to below the ECB target, then the current conditions are attractive. From an investor perspective it’s the perfect hedge if the opposite happens and they can also get exposure to inflation."

If conditions allow, the product could also get more strategic for issuers in their attempt to increase their ESG supply. France is certainly considering a green linker.

“It is not innovation for innovation’s sake. It is also reflecting a lot of demand that we have collected from investors over the past few months," said Benjamin de Forton, an SSA banker at BNP Paribas, referring to a potential French green linker.

"It is natural for this type of product to appear in the market and it is almost strange that no one has done it. It’s a very healthy debate that we are having and I think it’s fair to say that at this stage we are collecting pretty tremendous feedback.”

Bank of America, Citigroup, HSBC, Societe Generale and UniCredit were the leads on the Italy deal. BNP Paribas, Citigroup, Credit Agricole, JP Morgan and Societe Generale were the leads on France's transaction.